There are as many theories about why and how the Great Depression ended as there are about how it began. The mainstream causes of “the most severe and protracted economic crisis in American history.”[1] include international factors such as inflation in Germany, the fragility of most European economies due to the Great War, high tariffs, and the U.S. recall of loans to Germany. Home-front factors were also to blame, including the stock market crash, banks’ recall of loans, and the failure of farms due to the Dust Bowl.

The theories about how this great economic crisis ended are as numerous. Many scholars argue that the New Deal, implemented by Roosevelt, ended it. Moreover, others believe it was World War II spending that single-handedly rescued Americans from it. More notable theories, such as the Keynesian (insufficient aggregate demand), the Austrian (credit expansion), and the Monetary or aggregate demand (rising money supply), provide a more comprehensive understanding of how it ended.

The latter theories agree that it was not a single factor, such as World War II spending, but rather multiple factors that contributed to ending the Great Depression. In agreement, Christina Romer states, “Plausible estimates of the effects of fiscal and monetary changes indicate that nearly all the observed recovery of the U.S. economy prior to 1942 was due to monetary expansion.”[2] The monetary interpretation, or aggregate demand, offers the most convincing explanation for the end of the Great Depression because it demonstrates that recovery began with renewed monetary expansion, while later fiscal measures reinforced and accelerated that improvement.

The monetary interpretation of the Great Depression holds that the downturn’s severity and duration were caused primarily not by private-market breakdowns but by a dramatic contraction of the money supply beginning in 1929 and by the Federal Reserve’s failure to provide adequate liquidity. Recovery, in this view, occurred only after sustained monetary expansion, with gold inflows and deliberate policy changes restoring aggregate demand.

(Above Image)Encyclopaedia Britannica. “Great Depression.” Last modified January 13, 2026. https://www.britannica.com/event/Great-Depression

A strong proponent of this theory is Christina Romer. She argues that the recovery began in 1933 and was driven primarily by expansionary monetary policy, including gold inflows, the abandonment of the gold standard, and credit expansion. In other words, it was these forces that stimulated investment, output, and consumption throughout the mid-1930s, thereby indicating that World War II spending and the New Deal helped stimulate but were not the initiators.

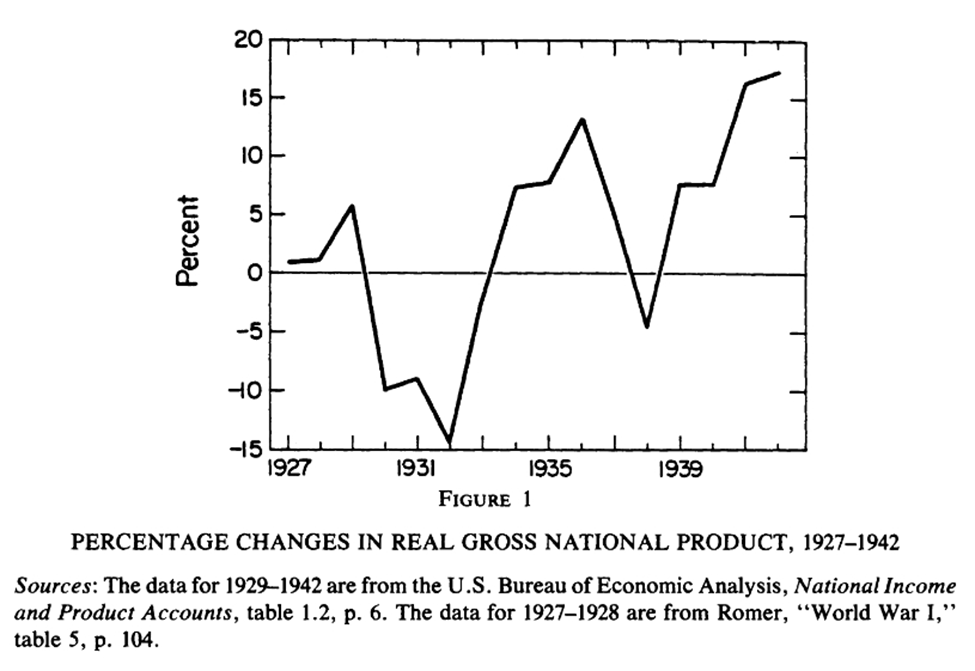

In support of this theory, evidence shows that the GNP had already been on the rise well before World War II and the New Deal were in play. In fact, Romer states, “Between 1929 and 1933, real GNP declined 35 percent; between 1933 and 1937, it rose 33 percent.”[3] The graph demonstrates that the economy was improving several years before World War II spending began. What of the New Deal? Beginning in 1933, many believe this fiscal force could have helped, and even was the driving force, putting Americans back to work. However, there is evidence that the employment rate was already on the rise, reaching levels seen in the early 1930s. Ben Bernanke and Martin Parkinson, in their article, believed that “the New Deal is better characterized as having ‘cleared the way’ for a natural recovery rather than as being the engine of recovery itself,”[4] as they recognized people were already going back to work.

The current trend in the Great Depression economy showed all the signs of recovery due to monetary expansion efforts, such as gold inflows, which greatly increased the money supply. Romer brings this to light when she says, “The source of the huge increases in the U.S. money supply during the recovery was a tremendous gold inflow that began in 1933.”[5] Those imports totaled “$758 million just in February and March of 1934.”[6]

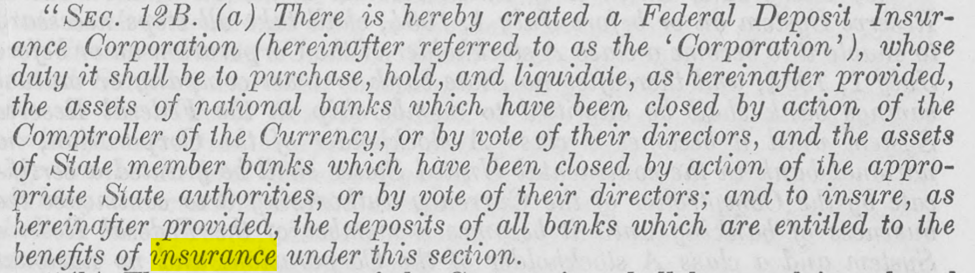

It needs to be said that this was not a natural self-correction but was created by the Roosevelt administration. After deliberately accumulating gold, Franklin D. Roosevelt chose not to sterilize the inflows, intending instead to allow them to expand the money supply and stimulate economic activity. As Christina Romer explains, “Although the later gold inflow was mainly due to political developments in Europe, the largest inflow occurred immediately following the revaluation of gold mandated by the Roosevelt administration in 1934.”[7] In addition, Roosevelt, through the Banking Act of 1933 (Glass–Steagall Act), created the Federal Deposit Insurance Corporation (FDIC). This separation of commercial from investment banking aimed to stop bank runs and stabilize deposits, thereby helping rebuild the money supply. The image below serves as an example of the government’s seeking to rebuild the monetary foundation of the economy.

Banking Act of 1933, Pub. L. No. 73-66, 48 Stat. 162 (June 16, 1933), Library of Congress.

In conclusion, while fiscal policy, structural change, and wartime mobilization all contributed to recovery, the weight of the evidence indicates that monetary expansion provided the decisive turning point, making the monetary interpretation the most persuasive explanation for the end of the Great Depression.

[1] Michael A. Bernstein, “The Great Depression as Historical Problem,” OAH Magazine of History 16, no. 1 (2001): 3, http://www.jstor.org/stable/25163480.

[2] Christina D. Romer, “What Ended the Great Depression?” The Journal of Economic History 52, no. 4 (1992): 1, http://www.jstor.org/stable/2123226.

[3] Romer, “What Ended the Great Depression?” 760.

[4] Ben Bernanke and Martin Parkinson, “Unemployment, Inflation, and Wages in the American Depression: Are There Lessons for Europe?” The American Economic Review 79, no. 2 (1989): 212, http://www.jstor.org/stable/1827758.

[5] Romer, “What Ended the Great Depression?” 773.

[6] Arthur I. Bloomfield, Capital Imports and the American Balance of Payments. (Chicago: University of Chicago Press, 1950), 145.

[7] Romer, “What Ended the Great Depression?” 781.

Jonathan White

Contact: whitejonathan173@gmail.com

Leave a comment